If everybody believed what everybody else believed, everybody would set the same price on everything. The middle-aged men on the stock exchange floor could quit hollering and go have lunch.

(PJ O’Rourke)

I have previously mentioned that there are 26 different variables which need to be considered in the valuation of a business. This flies in the face of “valuations” which take the profit of a business, and apply a standard multiplier without regards for other circumstances. Let me prove to you why this stand alone simple multiplier approach guarantees to rob someone; buyer or seller.

The basis for a multiplier approach is that the valuer takes one of: the monthly net profit before tax, the net profit after tax, or the free cash flow of a business and multiplies the number by 20 (usually). There are various theories on which one of NPBT, NPAT or FCF to use, depending on how many mirrors, and how much smoke is used. Some even use sales turnover as the basis! More on that on another day.

The theory goes that the more the business is making (or the owner is able to remove for himself) the more the business is worth. I have no real problem there, but the straight line relationship is a problem. If a business is making no money, it is therefore worth nothing, according to this approach. Really? Well if one listens to these guys, yes.

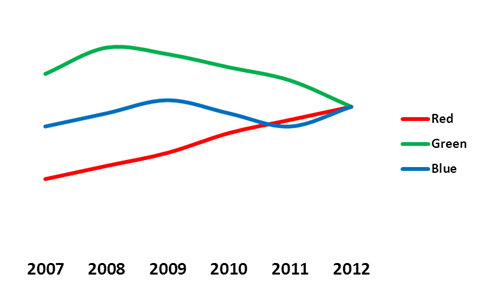

By the same token, a business which reported a profit of R100,000 at the end of last month is worth twice that of a business which made R50,000 in the same month? No, actually; Not even these valuation methods are that simplistic. They will take the average for the last twelve months if they have a modicum of self respect. But that too, is problematic. Take a look at this illustration of profits:

Which business would you prefer to invest in?

The red business has been rising nicely through the years, reporting constantly rising returns for its owners. The blue company, on the other hand, while it has the same profit in the last year as the red company, has a very different history. How does one ever place the same value on the two companies? To compound the problems of this theory, the green company will be apportioned the same value, despite the fact that its fortunes have been waning for some years.

Remember that these are annual figures in the illustration, so the monthly average has been taken care of. Of course there cannot be a straight line correlation between their values and their profits.

“Tarmstwenty” protagonists will often call into effect an average of the last three years. Well that compounds the error even further. Simple mathematics (for those with an average above 13% in grade 7) decrees that in this approach will work against red (gaining momentum) and for a weakening green.

Do yourself a favour – get the job done professionally. Rather you know well in advance what you are going to be up against in the sale of your business, than you find out when it is too late. Find out more about professional business valuations.